Week of April 27, 2026 in Review

The Fed left rates unchanged, while inflation climbed on higher gas prices. National home values rose for a seventh straight month, and new construction showed mixed signals. Here are the key takeaways.

- Fed Holds Rates Steady Amid Growing Policy Debate

- Rising Oil Prices Push Inflation Higher

- Appreciation Highlights Homeownership Benefits

- Housing Starts Beat Expectations, Permits Pull Back

- In Focus: GDP and Unemployment

- Family Hack of the Week

- What to Look for This Week

- Technical Picture

Fed Holds Rates Steady Amid Growing Policy Debate

As expected, the Federal Reserve left its benchmark Federal Funds Rate unchanged at 3.50% to 3.75%, marking its third straight meeting without a change after cuts late last year. While this rate doesn’t directly determine mortgage rates, it plays a major role in shaping borrowing costs across the economy.

What’s the bottom line? Although the pause was widely anticipated, the decision revealed growing division within the central bank, with four officials dissenting – the highest number in decades. One favored an immediate rate cut, while others pushed back on signaling that cuts are likely ahead, even as they agreed to hold rates steady for now.

This split reflects the Fed’s ongoing balancing act: inflation is still above target, while some signs point to a cooling job market. Add in global uncertainties, and it’s clear policymakers are proceeding carefully.

In his remarks, Jerome Powell also shared that he plans to remain on the Federal Reserve Board as a Governor after his term as Chair ends in May.

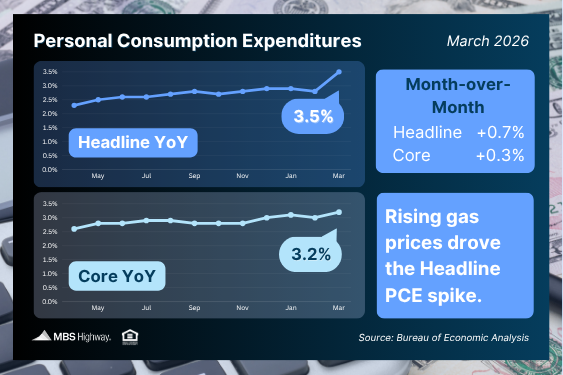

Rising Oil Prices Push Inflation Higher

Headline Personal Consumption Expenditures (PCE) rose 0.7% in March, driven largely by a surge in gas prices tied to Middle East tensions, lifting the annual rate to 3.5%. The Fed’s preferred inflation measure, core PCE (which excludes food and energy), increased a more moderate 0.3%, with the annual rate at 3.2%.

What’s the bottom line? Inflation is still running above target, reinforcing the Fed’s cautious approach. It also helps explain why some policymakers are in no rush to cut rates as they weigh mixed signals across the economy.

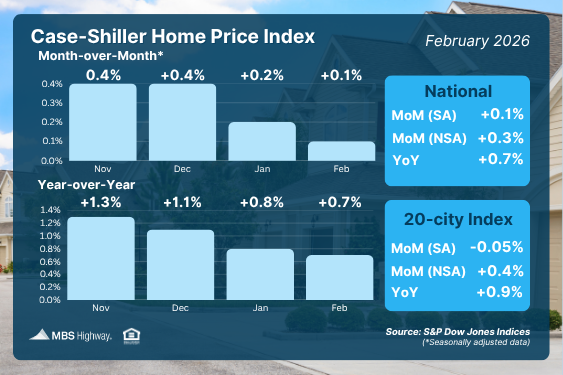

Appreciation Highlights Homeownership Benefits

U.S. home values edged up from January to February, rising 0.3% before seasonal adjustments and 0.1% after, according to the Case-Shiller Home Price Index. Year over year, prices are up 0.7%.

Data from the Federal Housing Finance Agency (FHFA) shows prices were mostly flat month over month (seasonally adjusted), with a stronger 1.7% annual gain for homes backed by conventional loans.

What’s the bottom line? Home prices have now increased for seven consecutive months, per Case-Shiller, at roughly a 3% annual pace. Even modest gains can make a difference over time. For instance, a $500,000 home appreciating at 3% would add about $15,000 in value in a year, underscoring the long-term wealth potential of homeownership.

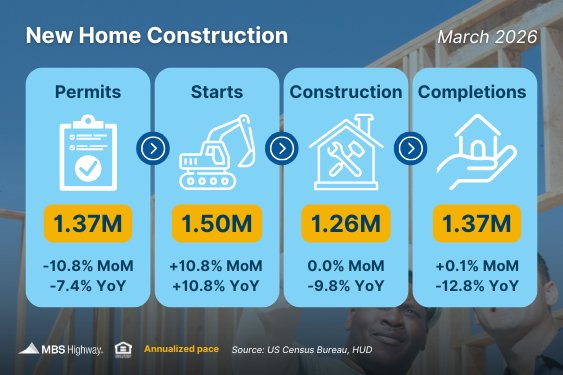

Housing Starts Beat Expectations, Permits Pull Back

Housing starts rose nearly 11% from February to March, as builders ramped up activity despite ongoing affordability challenges. Gains were seen in both single-family and multi-family construction, likely supported by better weather.

At the same time, building permits fell by a similar margin, an early sign that future construction activity may slow.

What’s the bottom line? While the jump in housing starts came in well above forecasts, the drop in permits suggests builders are still proceeding carefully amid ongoing economic and geopolitical uncertainty.

In Focus: GDP and Unemployment

The first estimate for Q1 2026 GDP shows the U.S. economy grew at an annualized rate of 2%, up from 0.5% in Q4, when a government shutdown weighed on activity late in the year. Growth in the first quarter was driven in part by AI-related investment and the rebound in government spending, while higher imports partially offset those gains.

Initial jobless claims fell by 26,000 to 189,000, and continuing claims declined by 23,000 to 1.785 million. Persistently low initial claims may suggest some unemployed workers are turning to gig work, which isn’t fully captured in these figures.

Family Hack of the Week

In honor of National Strawberry Month, enjoy this Strawberry Peach Crumble courtesy of Food Network. This refreshing dessert serves 4 to 6.

Preheat your oven to 350 degrees Fahrenheit. Butter an 8-by-8-inch glass baking dish and set aside.

In a medium bowl, whisk together 2 tablespoons lemon juice and 1 1/2 teaspoons arrowroot flour until smooth. Add 1 pound halved strawberries, 1 1/2 pounds peeled, pitted, and sliced peaches, and 1/2 cup light brown sugar, then gently toss until the fruit is evenly coated. Pour the mixture into the prepared dish.

To make the topping, combine 2/3 cup all-purpose flour, 2/3 cup old-fashioned oats, 1/2 cup sliced almonds, 1/4 cup light brown sugar, 1 teaspoon cinnamon, and 1/4 teaspoon sea salt in a food processor and pulse to mix. Add 1 stick chilled unsalted butter, cut into small cubes, and pulse again until the mixture resembles coarse crumbs with pea-sized pieces of butter.

Sprinkle the topping evenly over the fruit and bake for 40 to 45 minutes, until the filling is bubbling and the top is lightly golden. Let the crumble cool for about 5 minutes before serving warm with whipped cream or your favorite ice cream.

What to Look for This Week

More housing updates are on the way, with New Home Sales data set for release on Tuesday. It’s also a key week for labor market insights. Job opening figures come out Tuesday, followed by private payroll data on Wednesday, weekly unemployment claims on Thursday, and Friday’s highly anticipated jobs report, featuring nonfarm payrolls and the unemployment rate.

Technical Picture

Mortgage Bonds ended last week testing a key ceiling around 100.61. If they can’t break above that level, there’s room to fall, with the next area of support near 100.35. Meanwhile, the 10-year Treasury continues to trade within a fairly wide range, with support around 4.33% and resistance near 4.48%.